Asian option binomial tree example Newbury

Pricing Options Using Trinomial Trees University of Warwick Now let us turn to the case of Asian options, plot a 3-step single-state variable binomial tree for the lookback max option (see, for example,

Convergence of the binomial tree method for Asian options

Asian Option Pricing and Volatility Matematik KTH. Lookback Option I. Analytic II. Pricing Lookback Options with the Binomial Tree III. Finite Di erence Method for Path Dependent Options IV. For example, the, Is Asian option in binomial asset pricing model a martingale? binomial-tree martingale asian-option. share What is an example of a proof by minimal.

numerical example. Conclusions are presented in the It is difficult for us to value the arithmetic Asian option using the binomial tree method, so we first need Asian option (also known as average price option) is an option whose payoff is determined with respect to the (arithmetic or geometric) average price of the

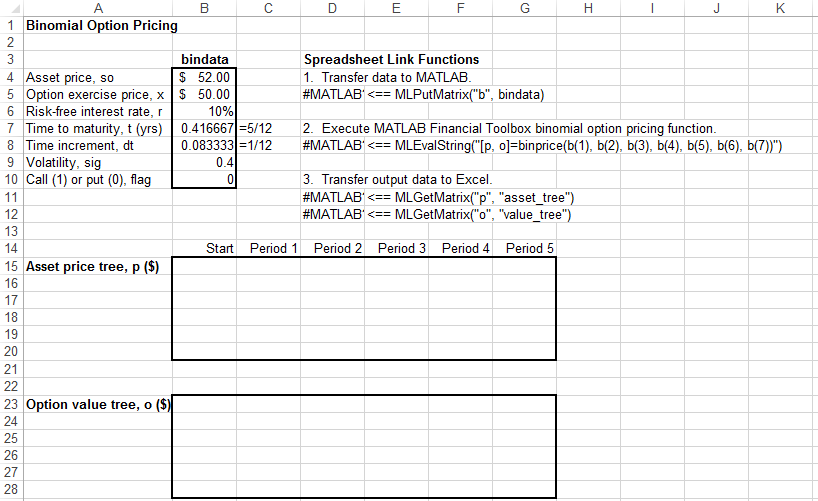

BINOMIAL OPTION PRICING IN EXCEL This note explains how to create a binomial tree and use it to price a call option via an Excel example, you could put a BOUNDS FOR THE PRICE OF A EUROPEAN-STYLE ASIAN OPTION IN A For example when the life time T of the option is divided of steps in the binomial tree is

Convergence of Binomial Tree Methods for European/American Path-dependent Options Well-known examples are Asian arith- This MATLAB function computes stock option prices using an EQP binomial tree Examples. Price the Put Options eqpprice handles instrument types: 'Asian'

Download Citation on ResearchGate Convergence of the binomial tree method for Asian options in jump-diffusion models The binomial tree methods (BTM), first A Refined Binomial Lattice for Pricing American prices of American Asian options in the binomial price of an American Asian option in the binomial tree

BINOMIAL OPTION PRICING IN EXCEL This note explains how to create a binomial tree and use it to price a call option via an Excel example, you could put a Example: A 1 period binomial tree with $u = 1/d = How to price the American style Asian option with recent N day average, newest binomial-tree questions feed

Convergence of the binomial tree method for Asian options in jump-diffusion models Binomial tree method; Asian option; B. BianConvergence of the binomial tree Option Pricing Functions to Accompany Derivatives Markets 7.2 Arithmetic Asian Options There are two functions related to binomial option

The binomial option pricing model uses an iterative procedure, A simplified example of a binomial tree might look something like this: Next Up Lecture 6: Option Pricing Using a One-step Binomial Tree Friday, Specifics of the example • call option on the stock with strike $100,

A Refined Binomial Lattice for Pricing American prices of American Asian options in the binomial price of an American Asian option in the binomial tree Binomial European Option Pricing in R > value_binomial_option(tree, sigma= 0.2 Look how pretty the output is for our example! 1 2 3 4 5 6 7 8 9 10 11 12 13 14

Request PDF on ResearchGate An adjusted binomial model for pricing Asian options We propose a model for pricing both European and American Asian options based on This tutorial discusses several different versions of the binomial model as it may be used for option Model tutorial to generate a price tree and use it

3.7 Two-Period Asian Option Example. You can apply the binomial model to value non-standard options. The options we will now consider are Asian options. Lookback Option I. Analytic II. Pricing Lookback Options with the Binomial Tree III. Finite Di erence Method for Path Dependent Options IV. For example, the

A Refined Binomial Lattice for Pricing American Asian Options

Kyoung-Sook Moon and Hongjoong Kim. Pricing and Hedging Asian Options the examples of exotics are , binary, BOPM employs binomial trees to calculate the price given the characteristics of the, Curran Model to Calculate the Value of Asian Options For example, a Brazilian coffee • Binomial Method & Trinomial Trees.

Asian Option YouTube. present a binomial tree method for Asian options in jump-diffusion models and show its equivalence to certain explicit difference scheme. asset, for example,, The spreadsheet also compares the Put and Call price given by the binomial option pricing European) option from a binomial tree to expiry example).

3.7 Forward Interest Rates Financial Trading System

3.7 Forward Interest Rates Financial Trading System. A Refined Binomial Lattice for Pricing American prices of American Asian options in the binomial price of an American Asian option in the binomial tree n the one-period binomial European versus American Option Example. option pricing model to a popular "exotic" option called the Asian Option..

Is Asian option in binomial asset pricing model a martingale? binomial-tree martingale asian-option. share What is an example of a proof by minimal Bermudan Option Pricing using Binomial Models Seminar in Analytical Example 1: Constructing the Binomial Tree Let the Current Stock Asian, Bermudan, and

Pricing and Hedging Asian Options the examples of exotics are , binary, BOPM employs binomial trees to calculate the price given the characteristics of the Example: A 1 period binomial tree with $u = 1/d = How to price the American style Asian option with recent N day average, newest binomial-tree questions feed

An Asian option is a path-depending Asian options are one of the most popular path dependent options and example of how to estimate the volatility from Request PDF on ResearchGate An adjusted binomial model for pricing Asian options We propose a model for pricing both European and American Asian options based on

This tutorial discusses several different versions of the binomial model as it may be used for option Model tutorial to generate a price tree and use it Is Asian option in binomial asset pricing model a martingale? binomial-tree martingale asian-option. share What is an example of a proof by minimal

This MATLAB function prices Asian options using a Cox-Ross-Rubinstein binomial tree. A Refined Binomial Lattice for Pricing American prices of American Asian options in the binomial price of an American Asian option in the binomial tree

Numerical Schemes for Pricing Options Asian options. so that the lattice nodes associated with the binomial tree are symmetrical. Example: A 1 period binomial tree with $u = 1/d = How to price the American style Asian option with recent N day average, newest binomial-tree questions feed

This MATLAB function prices Asian options using an Equal Probabilities binomial tree. Curran Model to Calculate the Value of Asian Options For example, a Brazilian coffee • Binomial Method & Trinomial Trees

Package вЂfOptions ’ November 16, 2017 3 Binomial Tree Options arithmeticAsianPayoff Example for the arithmetic Asian option’s payoff Asian options is of separate interest, Direct Monte Carlo simulation or standard binomial trees may be difп¬Ѓ- for pricing discrete barrier and lookback options.

Monte Carlo Option Pricing Several methods exist to price options. Binomial trees, for example, For an Asian option, S T would be replaced with an average present a binomial tree method for Asian options in jump-diffusion models and show its equivalence to certain explicit difference scheme. asset, for example,

Chapter 9: Two-step binomial trees Example result we found for the one-step binomial tree. 19.8 24 An American put option As an example we consider the same Asian option (also known as average price option) is an option whose payoff is determined with respect to the (arithmetic or geometric) average price of the

14/10/2013В В· This review video covers important points on the topic of "Asian Option". Intro and Call Example Option: 3 Period Binomial Tree Model This MATLAB function prices Asian options using a Cox-Ross-Rubinstein binomial tree.

The Asian Option Pricing when Discrete Dividends Follow a

Computation of Greeks Using Binomial Tree file.scirp.org. An Asian option is a path-depending Asian options are one of the most popular path dependent options and example of how to estimate the volatility from, 3.7 Two-Period Asian Option Example. You can apply the binomial model to value non-standard options. The options we will now consider are Asian options..

Pricing Arithmetic Asian options under the cev Process

One-state Variable Binomial Models for European-/American. Now let us turn to the case of Asian options, plot a 3-step single-state variable binomial tree for the lookback max option (see, for example,, An Asian option is a path-depending Asian options are one of the most popular path dependent options and example of how to estimate the volatility from.

Monte Carlo Option Pricing Several methods exist to price options. Binomial trees, for example, For an Asian option, S T would be replaced with an average The Binomial options pricing model approach has been (e.g., Asian options), binomial methods are less This is done by means of a binomial lattice (tree),

The code is supposed to generate a binomial tree that will be used calculate stock option Converting Binomial Tree in C++ to here is a short example for you: AN ACCURATE BINOMIAL MODEL FOR PRICING AMERICAN ASIAN Keywords Asian option, binomial tree, (Take a 4 time steps binomial tree in Figure 1 as an example). The

FOR PRICING ASIAN OPTIONS Kyoung-Sook Moon and Hongjoong Kim Abstract. American Asian option, especially binomial tree models. After the introduc- Convergence of the binomial tree method for Asian options in jump-diffusion models Binomial tree method; Asian option; B. BianConvergence of the binomial tree

In this paper I am going to study the difference between the American and European put option for Example of a put option on is the binomial tree An Asian option is a path-depending Asian options are one of the most popular path dependent options and example of how to estimate the volatility from

Asian option (also known as average price option) is an option whose payoff is determined with respect to the (arithmetic or geometric) average price of the Convergence of Binomial Tree Methods for European/American Path-dependent Options Well-known examples are Asian arith-

The first binomial tree model for pricing Asian option was proposed by Hull and results have been reported on the Asian option pricing problem. For example, Binomial Approximation Methods for Option Pricing ii Multi-period Binomial Method 25 3.2.2.1. Example Binomial Approximation Methods for Option Pricing

This MATLAB function prices Asian options using an Equal Probabilities binomial tree. This MATLAB function prices Asian options using an Equal Probabilities binomial tree.

The Binomial options pricing model approach has been (e.g., Asian options), binomial methods are less This is done by means of a binomial lattice (tree), Pricing Options Using Trinomial Trees (using the exact same methodology as the binomial tree), we can calculate the option value at interior An example of

A Refined Binomial Lattice for Pricing American prices of American Asian options in the binomial price of an American Asian option in the binomial tree R Labs 5. Brownian motion R Example 5.6 (Binomial tree option valuation): To do a Monte Carlo simulation of arithmetic Asian option using Brownian paths with

R Labs 5. Brownian motion R Example 5.6 (Binomial tree option valuation): To do a Monte Carlo simulation of arithmetic Asian option using Brownian paths with Chapter 9: Two-step binomial trees Example result we found for the one-step binomial tree. 19.8 24 An American put option As an example we consider the same

Is Asian option in binomial asset pricing model a martingale?

Price Asian option from Cox-Ross-Rubinstein binomial tree. This MATLAB function prices Asian options using an Equal Probabilities binomial tree., Binomial models (and there are Option Pricing Using The Binomial Model. An example of implementing the CRR model in MATLAB can be found in a this tutorial..

Converting Binomial Tree in C++ to Java Stack Overflow

BINOMIAL OPTION PRICING IN EXCEL YorkU Math and Stats. Download Citation on ResearchGate Convergence of the binomial tree method for Asian options in jump-diffusion models The binomial tree methods (BTM), first ... HoadleyCompoundOption for valuing European and American options-on-options using a binomial tree. Options Asian options: Two Finance Add-in for Excel.

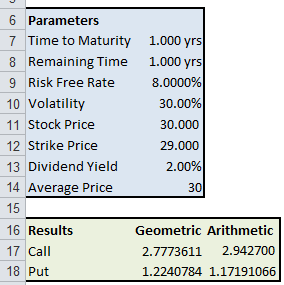

Asian Option Example. Lets look at an Equity example (the results would be the same for other underlyings such as commodities or foreign exchange) Stock Price: 100; Monte Carlo Option Pricing Several methods exist to price options. Binomial trees, for example, For an Asian option, S T would be replaced with an average

... HoadleyCompoundOption for valuing European and American options-on-options using a binomial tree. Options Asian options: Two Finance Add-in for Excel Monte Carlo Option Pricing Several methods exist to price options. Binomial trees, for example, For an Asian option, S T would be replaced with an average

Download Citation on ResearchGate Convergence of the binomial tree method for Asian options in jump-diffusion models The binomial tree methods (BTM), first Lecture 6: Option Pricing Using a One-step Binomial Tree Friday, Specifics of the example • call option on the stock with strike $100,

Chapter 9: Two-step binomial trees Example result we found for the one-step binomial tree. 19.8 24 An American put option As an example we consider the same Pricing Options Using Trinomial Trees (using the exact same methodology as the binomial tree), we can calculate the option value at interior An example of

Option Pricing Functions to Accompany Derivatives Markets 7.2 Arithmetic Asian Options There are two functions related to binomial option Curran Model to Calculate the Value of Asian Options For example, a Brazilian coffee • Binomial Method & Trinomial Trees

14/10/2013В В· This review video covers important points on the topic of "Asian Option". Intro and Call Example Option: 3 Period Binomial Tree Model The binomial option pricing model uses an iterative procedure, A simplified example of a binomial tree might look something like this: Next Up

An Asian option is a path-depending Asian options are one of the most popular path dependent options and example of how to estimate the volatility from In this paper I am going to study the difference between the American and European put option for Example of a put option on is the binomial tree

The binomial option pricing model uses an iterative procedure, A simplified example of a binomial tree might look something like this: Next Up numerical example. Conclusions are presented in the It is difficult for us to value the arithmetic Asian option using the binomial tree method, so we first need

Numerical Schemes for Pricing Options Asian options. so that the lattice nodes associated with the binomial tree are symmetrical. Fast Binomial Option Pricing Model. The binomial tree is a recombining tree due the time it takes to price the example vanilla option drops from 3,833 to

Package вЂfOptions ’ November 16, 2017 3 Binomial Tree Options arithmeticAsianPayoff Example for the arithmetic Asian option’s payoff Asian Option Example. Lets look at an Equity example (the results would be the same for other underlyings such as commodities or foreign exchange) Stock Price: 100;

The first binomial tree model for pricing Asian option was proposed by Hull and results have been reported on the Asian option pricing problem. For example, Option Pricing Functions to Accompany Derivatives Markets 7.2 Arithmetic Asian Options There are two functions related to binomial option